Performance Equity Compensation Design and Use Matrix

•

3 likes•4,777 views

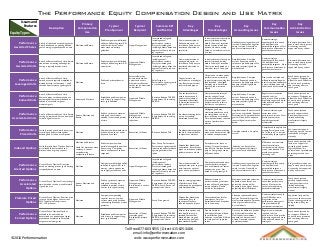

This matrix describes the 11 types of performance-based equity compensation and 9 key issues (primary use, primary plan sponsor, typical recipient, common KPI, key advantages and disadvantages, accounting, communication and administration issues).

Recommended

Recommended

More Related Content

Viewers also liked

Viewers also liked (11)

More from PERFORMENSATION

More from PERFORMENSATION (20)

Recently uploaded

Recently uploaded (20)

Performance Equity Compensation Design and Use Matrix

- 1. The Performance Equity Compensation Design and Use Matrix ©2016 Performensa0on Toll free 877-‐803-‐9255 | Direct 415-‐625-‐3406 email: info@performensa0on.com web: www.performensa0on.com Descrip(on Primary Compensa(on Use Typical Plan Sponsor Typical Recipient Common KPI and Metrics Key Advantages Key Disadvantages Key Accoun(ng Issues Key Communica(on Issues Key Administra(on Issues Performance Awarded Shares Award of restricted outstanding shares. Award size based on meeting defined goals. Vesting is typically based on time Motivate and Retain Public companies with limited ability to define long-term KPI and metrics,but a need to meet stock ownership guidelines Upper Management Internal and soft goals, including annual performance reviews. Project oriented goals including delivery dates and approvals of new products by regulators Communicates value of equity awards prior to award date.Fairly easy to translate dollar value to award size In down times awards may be severely limited providing little in the way of retention. Award creates immediate dilution.Goals are usually based on a maximum term of one-year Liability accounting until award is made. Fixed accounting after award is made. Generally no need for valuation services Communicating a hypothetical future award can be difficult and potentially dangerous.Most performance orientation is generally shorter-term Pre-award information not kept in stock admin system. Accounting not fully supported by any system Performance Awarded Units Award of Restricted Stock Units.Award size based on meeting defined goals. Vesting is typically based on time Motivate and Retain Public companies with limited ability to define long-term KPI and metrics Upper and Middle Management Internal and soft goals, including annual performance reviews. Project oriented goals including delivery dates and approvals of new products by regulators Communicates value of equity awards prior to award date.Fairly easy to translate dollar value to award size In down times awards may be severely limited providing little in the way of retention. Goals are usually based on a maximum term of one-year SimpleValuation. Complex accrual. Expense booked is relative to probable payout.No expense reversal if goals are market based Communicating a hypothetical future award can be difficult and potentially dangerous. Most performance orientation is generally shorter-term Pre-award information not kept in stock admin system. Accounting not fully supported by any system Performance Leveraged Units Award of Restricted Stock Units. Spread at vest is typically multiplied or divided by factors of between 1 and 5, (based on performance against goals) Motivate Public and private financial firms Sales staff,market drivers,business-line owners and others where direct financial results can be associated to individuals SalesTargets or Performance against growth or revenue goals Top performers are rewarded in a meaningful way. Bottom performers receive limited payout Corporate or market under- performance may result in top performers receiving less than intended. Leveraged multiples must be revisited regularly and monitored closely SimpleValuation. Complex accrual. Expense booked is relative to probable payout.No expense reversal if goals are market based Plans can be complex and difficult to explain.Regular, interim communications are a must.Unlikely to be fully understood by shareholders Stock admin systems do not support.Dividends are difficult to track.Difficult to correctly track proximity and remaining effort to reach goals Performance Earned Units Award of Restricted Stock Units. Shares at payout are determined as a percentage of shares awarded,and as related to threshold,target or maximum goals Attract and Motivate Established public companies with history to support long- term goal definition Upper and Middle Management Revenue,RelativeTSR,EPS, Recruitment,Cost-cutting, EBITDA Can set thresholds to ensure payout even if performance is below expectations Excellent communication tool for high performance Complex combinations of metrics and goal levels require intensive analysis. Improper design or poor performance can result in staff loss to competitors SimpleValuation. Complex accrual. Expense booked is relative to probable payout.No expense reversal if goals are market based Regular communication required to drive performance.Must provide proximity to goal and what still needs to be done to attain goals Stock admin systems do not support.Dividends are difficult to track.Difficult to correctly track proximity and remaining effort to reach goals Performance Accelerated Units Award of Restricted Stock Units.Award vesting is time-based,but can be moved forward if goals are met Attract,Motivate and Retain Public or private companies with goals that are best attained in shortened periods of time Upper and Middle Management. Broad-based in certain industries Revenue,RelativeTSR,EPS, Recruitment,Cost-cutting, EBITDA Provides motivating factor on top of standard Restricted Stock Units Misaligned goals may accelerate awards too early, providing little or no long- term incentive or retention. Time-based element reduced optics of performance metrics SimpleValuation. Basic accrual if goals are not probable. Expense acceleration if it is probable that goals will be met.No expense reversal if goals are market based Communication may be easier than other performance awards. Must provide resource for explaining potential acceleration Stock admin systems partially support these. Participant reports are limited and vesting acceleration is largely manual Performance Priced Units Variable-priced units.Award price is set according to performance against defined goals or index of companies Motivate Companies with volatile stock prices where over or under payout is a concern Executives (C-Suite) Revenue,RelativeTSR Provides moderate payout vehicle for unpredictable companies or markets Can be seen as demotivating when price becomes too high in relation to expectations Complex valuation. Complex accrual Complicated to explain and manage.Participants must be "in the loop" to truly be motivated by these types of plans No systematic support. Reporting must be custom created and managed manually Indexed Op(ons Variable-priced Stock Options. Exercise price linked to performance to a present index or group of peers Motivate andAttract. Useful for attraction when company is seen as outperforming competitors in future Public companies where performance against peers has been strong. Companies where over-payout has been suspected Executives (C-Suite) Peer Group Performance, Performance against specific industry index,Performance against general market index Shareholder friendly and understood. Ensures that payout is relative to market performance as a whole Participants view these as limiting. Over-performance may result in less than desired payout. Peer groups can be difficult to define Valuation can be complex. Accrual is generally simple if goals are clearly understood Difficult to communicate the value relative to competitor awards if they are not also indexed.Can provide competitor recruiting tool Stock admin systems offer little or no support for variable-priced options. Typically all admin is performed on spreadsheets between grant and vest dates Performance Granted Op(ons Grant of Stock Options.Grant size based on meeting pre-set goals. Vesting is typically based on time Motivate Companies with limited ability to define long-term KPI and metrics, where options are more highly valued than units Upper Management Internal and soft goals, including annual performance reviews. Project oriented goals including delivery dates and approvals of new products by regulators Communicates value of equity awards prior to grant date.Improves optics of grant size to participants Complex formula needed to convert performance goal into a combination of shares and exercise price. Not based on a long-term goal Liability accounting until award is made. Fixed accounting after award is made. Generally no need for valuation services Communicating a hypothetical future award can be difficult and potentially dangerous. Performance orientation is generally short-term Pre-grant information not kept in stock admin system. Accounting not supported well by any system Performance Accelerated Op(ons Grant of Stock Options.Grant vesting is time-based,but can be moved forward if goals are met Attract,Motivate and Retain Public or private companies with goals that may be achieved in periods of time shorter than typical vesting Upper and Middle Management. Broad-based in certain industries Revenue,RelativeTSR,EPS, Recruitment,Cost-cutting, EBITDA,Stock Price over given period of time Ensures vesting regardless of performance.Easily understood by participants with little downside Reduces impact of performance on grant since shares will vest if participant remains eligible. Double hurdle for participants May require complex valuation. Expense may be less due to potentially shortened life. Expense may be higher due to potentially fewer forfeitures Communication is easier than other performance awards. Must provide resource for explaining potential acceleration Stock admin systems partially support these. Participant reports are limited and vesting acceleration is largely manual Premium Priced Op(ons Grant of Stock Options. Exercise price is set to a price higher than current FMV. Typical plans set price at a 10%-15% premium Motivate Companies emphasizing superior returns,or when current stock price has been reduced significantly by market pressures Upper and Middle Management Stock Price growth Shareholder friendly and understood.Easy to administer.May have reduced expense impact Creates double hurdle for participants. Very low perceived value until options are in the money Valuation requires additional analysis. Potentially longer life may increase expense.Spread at time of grant reduces value. Accrual is basic Communication is easy at grant.Difficult as time progresses,unless performance meets goals. Can provide basis for competitor recruitment Supported fairly well by most stock admin systems. Optics showing growth to being in-the-money are limited Performance Earned Op(ons Grant of Stock Options.Options available to be exercised are determined as a percentage of total granted and as related to threshold, target or maximum goals Motivate Established public companies with history to support long- term goal definition Executives (C-Suite) (complex goals). Broad-based (simple goals) Revenue,RelativeTSR,EPS, Recruitment,Cost-cutting, EBITDA,Stock Price over given period of time Ensures that options only vest if performance is attained.Shareholder friendly.Payout in good situations can be higher than standard options Double hurdle for participants.May be difficult to set effective goals. Valuation is complex.Difficult to track pools of approved shares Cost of plan difficult to predict until all variables are known. Goal type drives whether expense can be reversed if missed.Generally requires complex valuation Regular communication required to drive performance.Must provide proximity to goal and what still needs to be done to attain goal Stock admin systems do not support.Difficult to correctly track proximity and remaining effort to reach goals Equity Types Issues and Features